Buying a house can feel out of reach. But with the right steps, you can make homeownership work for you. In this guide, you’ll learn how to improve your credit rating, save effectively, explore assistance programs, and choose mortgage options. We’ll also share data on mortgage rates and housing affordability, and show you how those trends affect what you pay.

Boosting Housing Affordability Through Credit Rating Improvements

Good credit opens doors to lower rates. A better credit score can save you thousands over a 30-year loan.

- Check your credit reports. Order free copies from AnnualCreditReport.com or other trusted credit rating agencies.

- Dispute errors. Mistakes can knock your score down—fix them fast.

- Lower credit utilization. Keep balances below 30% of each limit.

- Automate payments. Never miss a due date.

- Keep old accounts open. Length of history matters.

Aim for a score of at least 620. Above 740 gets you top-tier rates.

Saving Strategies for Your Down Payment

A solid savings plan builds confidence—and a down payment.

- Set a monthly target. Treat savings like a recurring bill.

- Cut non-essentials. Cancel subscriptions you rarely use.

- Use windfalls. Tax refunds, bonuses, or gifts go straight to savings.

- High-yield accounts. Park your cash where it earns more interest.

Example: Saving $300 per month plus a 2% APY can net over $11,000 in three years.

Gifts and Grants: Leveraging Family Help

Family or friends can jump-start your down payment.

- Gift letters. Lenders need a signed letter stating there’s no repayment requirement.

- Match programs. Some banks match family gifts up to a limit.

- Gift of equity. When buying from family, equity in their home can count toward your down payment.

Always get gift documentation early so your lender can review it.

Down Payment Assistance Programs

Many states and cities offer grants and low-interest loans to buyers.

- State Housing Finance Agencies. Check your state’s HFA website.

- Community Development Block Grants (CDBG). Federal money is funneled to local programs.

- Nonprofits. Organizations like NeighborWorks® help with first-time buyer grants.

- Employer-assisted housing. Some companies offer down-payment support.

Tip: Eligibility often depends on income limits and home price caps. Apply early, as funding can run out.

Understanding Credit Approval and Pre-Approval

Getting pre-approved shows sellers you mean business. It also gives you a clear budget.

- Gather documents. Pay stubs, W-2s, bank statements, tax returns, and ID.

- Shop around. Compare rates and fees from multiple lenders.

- Submit pre-approval. You authorize a hard credit pull.

- Receive your letter. Valid for 60–90 days

Pre-approval isn’t final approval. Rates and debts can still change before closing.

Navigating the Mortgage Process with CMG Home Loans

Working with the right lender makes a difference. Our partner, CMG Home Loans, offers:

- Fast pre-approval. Get a decision in 24–48 hours.

- Local underwriting. Decisions made near you, not overseas.

- Flexible rate locks. Lock for 30, 45, or 60 days.

- Low-down options. Programs for 3% or even 0% down for qualifying buyers.

Here’s how it works:

- Initial consult. A loan officer reviews your goals.

- Online application. Secure portal makes paperwork breezy.

- Document upload. Snap photos of pay stubs and bank statements.

- Pre-approval letter. Use it when house-hunting.

- Rate lock. When you find a home, choose your timing.

- Closing. Final docs get signed, keys get handed over.

CMG Home Loans has helped first-time buyers for over 35 years. They offer FHA, VA, USDA, and conventional loans.

Mortgage Options Explained

Your choice of loan matters for payment, down payment, and rate.

1. Conventional loans

- Backed by Fannie Mae/Freddie Mac.

- Down payment: 3–20%.

- Credit score: 620+ (better scores = lower PMI).

2. FHA loans

- Government-insured.

- Down payment: 3.5%.

- A credit score: 580+ qualifies for the best terms.

3. VA loans

- For veterans, active service members, and spouses.

- Down payment: 0%.

- No PMI required.

4. USDA loans

- For rural and some suburban homes.

- Down payment: 0%.

- Income limits apply.

5. Adjustable-Rate Mortgages (ARMs)

- Lower initial rate for 5, 7, or 10 years.

- Then adjusts annually.

- Good if you plan to sell or refinance before the adjustment.

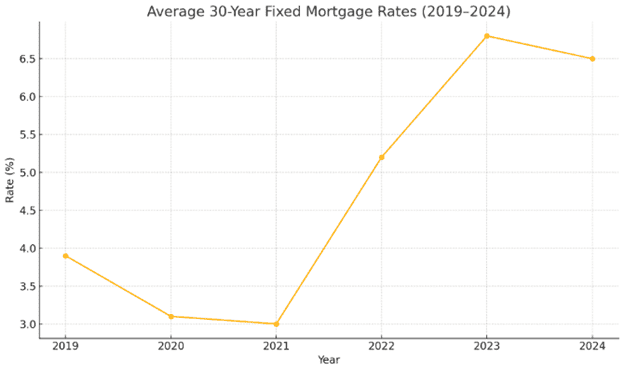

How Mortgage Rates Affect Your Payments

Rates change over time. This line chart shows the average 30-year fixed rates from 2019 to 2024 (data: Freddie Mac).

Even a half-point change can add $50–$75 to your monthly payment on a $300,000 loan.

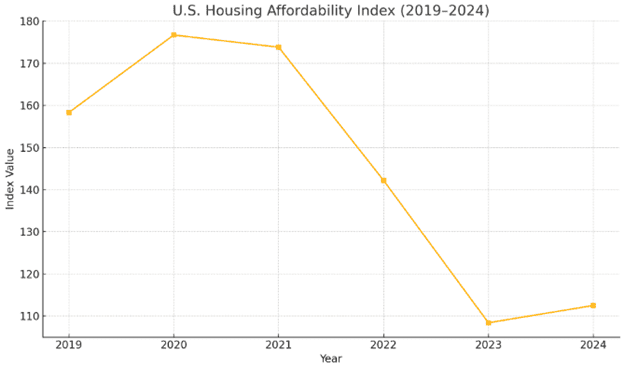

The State of Housing Affordability

Housing affordability measures whether a typical family can buy a median-priced home.

After peaking in 2020, affordability declined as prices climbed faster than incomes and rates. The slight uptick in 2024 shows stabilization, but the index remains below the 10-year average of 150.

Other Cost Factors to Budget

A home purchase has more than just the mortgage payment:

- Closing costs. 2–5% of the loan amount (appraisal, title, attorney, taxes).

- Home inspection. $300–$600.

- Property taxes & insurance. Plan for escrow payments.

- HOA fees. If you buy a condo or a planned community.

- Maintenance fund. Save 1–2% of home value per year for repairs.

Working with Your Real Estate Agent

Your agent guides you through the search, offers, and negotiations.

- Share your pre-approval. It sets realistic expectations.

- Set house-hunting goals. Must-haves vs. nice-to-haves list.

- Stay flexible. The perfect home may require compromise.

For more on choosing an agent, visit our buyer’s webpage.

First-Time Buyer Programs and Credits

- FTHB tax credit. Some states offer a state tax credit for first-time buyers.

- Mortgage credit certificates (MCC). Lowers your federal tax liability.

- Good Neighbor Next Door. HUD program for teachers, firefighters, and law enforcement.

Check with local housing agencies for current offers.

Recap and Next Steps

And that’s how you afford a house:

- Improve your credit rating.

- Save with a clear plan and lean on gifts or grants.

- Get pre-approved and set your budget.

- Explore assistance programs in your area.

- Pick the best mortgage type: conventional, FHA, VA, USDA, or ARM.

- Work with CMG Home Loans for fast, local service.

- Budget for all costs—closing, taxes, insurance, and maintenance.

With a clear plan and the right partners, buying your first house becomes achievable. Good luck!

Resources:

- Consumer Financial Protection Bureau – Credit Reports

- Fannie Mae – First-Time Homebuyers

- U.S. Department of Housing and Urban Development

- National Association of Realtors

Connect