Wondering what house you can afford in today's market? Whether you're a first-time home buyer or looking for your next move, understanding your budget is one of the most important steps in the process.

As you begin your home buying journey, working with the right mortgage lender can make understanding your budget much easier. The Masiello Group partners with CMG Home Loans to provide buyers with access to experienced loan officers who can explain financing options, answer questions, and guide them through the mortgage process from pre-approval to closing.

Keep reading to discover the key factors that influence affordability and how to determine a comfortable home-buying price range.

WHAT DETERMINES HOW MUCH HOUSE YOU CAN AFFORD?

When asking yourself, “how much house can I afford?” it is important to understand that there is not one simple answer, there are multiple factors that fit into this question:

-

Income and employment stability

-

Monthly payment obligations

-

Student loans

-

Car payments

-

Credit card payments

-

Credit score and credit history

-

Savings available

-

Down payment

-

Closing costs

-

Emergency fund

-

Interest rates

-

Property taxes, insurance, and housing costs

INCOME AND EMPLOYMENT STABILITY

Income is one of the leading factors in determining your budget for your next home. Consistent employment and income help demonstrate your ability to make monthly mortgage payments. Whether you work on salary, commission, hourly, or self-employment, lenders want to see a reliable source of income and financial stability.

If you're unsure how your income or employment situation may affect your buying power, speaking with a mortgage professional early in the process can provide valuable insight. An experienced loan officer can review your financial picture and help you understand what price range may be realistic before you begin searching for a home.

MONTHLY PAYMENT OBLIGATIONS

Your existing debt can impact how much house you can afford. It can affect how much room you have in your budget for a mortgage payment. Lenders will evaluate recurring payments such as:

-

Student loans: These can significantly affect your debt-to-income ratio, especially if you have large balances or high monthly payments.

-

Car payments: Auto loans are considered fixed monthly obligations and directly reduce the amount of income available for housing expenses.

-

Credit card balances: Lenders typically use the minimum monthly payment when calculating your debt, but high balances can still signal financial strain.

-

Personal loans: Any installment loans, such as personal or consolidation loans, are included in your monthly debt calculations.

The more debt you carry, the less income is available for housing expenses. This is why paying as much debt as possible before purchasing a home can improve affordability and increase your buying power. Reducing or eliminating smaller debts can make a noticeable difference in how much you qualify to borrow.

CREDIT SCORE AND CREDIT HISTORY

Credit score helps lenders assess risk, and this plays a key role in establishing the interest rate you receive. If your credit score is higher, you may qualify for a lower mortgage rate, which can reduce the monthly payment and increase how much house you can afford.

In addition to your credit score, lenders will also consider the credit history of the person who wants to take a loan to get information on how the individual handles their debts. These include your payment record, the percentage of credit used, the number of years since you opened your first credit account, and negative aspects like delinquency, collection activity, and bankruptcy.

SAVINGS AVAILABLE

Buying a home requires more than just a down payment. Having savings set aside demonstrates financial preparedness and can provide peace of mind after closing. Buyers should consider funds for:

-

Down payment costs: This is usually a percentage of the cost of the house and varies based on the kind of financing. High down payments can help lower your monthly payments and save you from having to pay private mortgage insurance.

-

Closing costs: This is made up of various fees from the lender, appraisals, title insurance, among others that you must pay during closing time. Closing costs usually range between 2%-5% of the cost of the home.

-

Moving costs: This involves moving to the new home, which can involve things like renting moving trucks, buying new furniture, and household items.

-

Savings for emergencies: It is vital to have some savings for future emergencies such as job loss or unexpected medical expenses.

-

Home maintenance and repair costs: Houses have costs related to maintenance and repair that you will need to account for when budgeting for owning your home. Some of these costs include HVAC service, replacement of appliances, roofing, etc.

It is advised to maintain your savings cushion in case of any surprises in the future.

INTEREST RATES

Mortgage interest rates have a direct impact on affordability. When interest rates rise, monthly mortgage payments increase, which can reduce purchasing power. On the other hand, lower interest rates may allow buyers to afford a more expensive home while keeping the same monthly payment.

Interest rates depend on several economic factors, such as inflation, the Federal Reserve's decisions, and the general market conditions. Even slight changes in interest rates have a substantial impact on your monthly payment and total financing.

For this reason, it is crucial for you to know about existing market conditions and consult a loan officer regarding interest rates' influence on your budget. A positive rate chosen properly can save you a lot of money.

PROPERTY TAXES, INSURANCE, AND HOUSING COSTS

Prospective homeowners tend to pay attention only to the cost of a house, while there are several other costs associated with being a homeowner, which should be considered when calculating the budget. They include:

-

Property taxes: These vary by location and are typically based on the assessed value of your home. They can increase over time and are often included in your monthly mortgage payment.

-

Homeowners insurance: This protects your home and belongings against damage or loss from events such as fire, storms, or theft. Costs can vary depending on location, coverage, and property value.

-

Private mortgage insurance (PMI), if applicable: Required for many loans when the down payment is less than 20%, PMI adds to your monthly payment but can often be removed once sufficient equity is built.

-

HOA fees: If your home is part of a homeowner's association, you may be required to pay monthly or annual dues that cover community maintenance and amenities.

-

Utilities: Ongoing costs such as electricity, water, gas, internet, and trash services should be included in your monthly budget.

-

Routine maintenance and repairs: Regular upkeep, such as landscaping, cleaning, and minor repairs, as well as larger projects like replacing appliances or fixing structural issues.

Considering these costs upfront can help create a more realistic budget and avoid any surprises after moving into your new home.

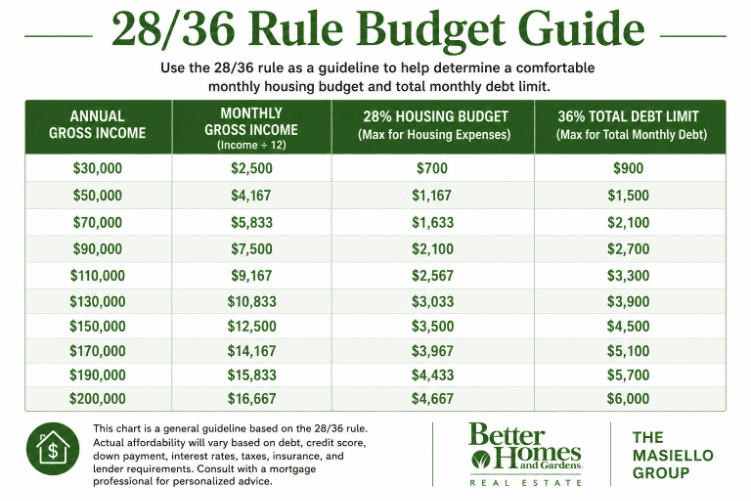

UNDERSTANDING THE 28/36 RULE

While every buyer's budget and spending ability is unique, the 28/36 rule is a good baseline for understanding how much house you can afford.

The rule suggests that:

-

No more than 28% of your gross monthly income should go toward housing expenses, including your mortgage payment, property taxes, homeowners' insurance, and any applicable HOA fees. This guideline helps ensure that your housing costs remain manageable and do not consume too much of your income, leaving room for other essential expenses.

-

No more than 36% of your gross monthly income should go toward your total monthly debt obligations, including your mortgage, car loans, student loans, credit cards, and other recurring debt payments. Staying within this limit helps maintain a balanced financial profile and reduces the risk of becoming overextended.

While the 28/36 rule is a helpful starting point, every buyer's financial situation is different. A mortgage professional can review your income, debts, savings, and financing options to provide a more personalized estimate of what you can comfortably afford.

Purchasing a home is one of the biggest financial decisions you'll make, and having knowledgeable professionals by your side can make the process much smoother. At the Masiello Group, we're proud to partner with CMG Home Loans to connect buyers with experienced mortgage professionals who can guide the financing process.

Whether you're purchasing your first home or your next home, getting pre-approved, understanding your financing options, and working with both a trusted real estate agent and lender can help you move forward with confidence.

Connect